Blog

Does Regulation E apply to Consumer Online Wire Transfers? Second Circuit to Hear Oral Argument on April 6, 2026

Published: Mar 31, 2026

On April 6, 2026, the United States Court of Appeals for the Second Circuit will hear oral argument in The People of the State of New York v. Citibank, N.A., Case No. 25-2105 (the “New York Case”), which presents a question of significant consequence for the financial services industry: does a wire transfer initiated by a consumer through a bank’s online banking service fall within the scope of the Electronic Fund Transfer Act ("EFTA") and its implementing regulation, Regulation E?

In January 2025, Judge J. Paul Oetken of the U.S. District Court for the Southern District of New York denied, in part, the Bank’s motion to dismiss the New York Attorney General's EFTA claims. The district court ruled that the EFTA and Regulation E applies to certain components of consumer wire transfers. This decision broke from decades of settled understanding and has already generated a split of authority among federal courts. The Second Circuit's decision is expected to have far-reaching implications for how banks handle consumer wire transfer disputes.

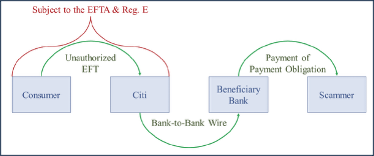

At the heart of the dispute was the interpretation of 15 U.S.C. § 1693a(7)(B), which provides that an "electronic fund transfer" does not include "any transfer of funds … made by a financial institution on behalf of a consumer by means of a service that transfers funds held at either Federal Reserve banks or other depository institutions and which is not designed primarily to transfer funds on behalf of a consumer."

The court adopted the Attorney General's theory (as depicted above) that a consumer wire transfer should be understood not as a single, end-to-end transaction, but as comprising at least three distinct components: (1) a transfer from the consumer to her bank, (2) an interbank transfer along the wire network, and (3) a transfer from the recipient's bank to the recipient. Under this framework, the court concluded that Section 7(B) excludes only the middle, bank-to-bank segment from EFTA coverage, leaving the consumer-to-bank component, specifically, the electronic payment order and resulting debit from the consumer's account, subject to EFTA's protections. The court found that the word "transfer" in subsection 7(B) refers narrowly to the movement of funds within a wire network, not the entire wire transfer from sender to ultimate recipient. In reaching its holding, the court acknowledged that the question was one of "first impression" and that Congress "might not have anticipated" this result.

The Appeal

On appeal, the Bank makes four primary arguments to support its position that the lower court was wrong.

First, the Bank contends that the ordinary and specialized meaning of "transfer of funds" refers to the complete, end-to-end movement of money from sender to recipient, not isolated segments of that journey. They argue that Section 7 of the EFTA treats enumerated examples, including point-of-sale transfers, ATM transactions, and direct deposits, as single, indivisible transfers, and that the same logic must apply to the wire-transfer exemption in Section 7(B).

Second, the Bank argues that the district court's interpretation renders Section 7(B) entirely superfluous, as the bank-to-bank portion of a wire transfer (the only component exempted under the lower court's reading) was never covered by EFTA in the first place because it does not involve consumer accounts.

Third, the Bank points to the 2010 Dodd-Frank Act, which extended certain EFTA protections to cross-border remittance transfers, a subset of consumer wire transfers. The Bank argues this amendment would have been unnecessary if EFTA already covered consumer wire transfers.

Fourth, the Bank argues that its interpretation is supported by decades of uniform regulatory guidance from the CFPB, the Federal Reserve, the OCC, the FDIC, and FinCEN, all of which have stated that consumer wire transfers are governed by Article 4A of the Uniform Commercial Code (“UCC”), not the EFTA or Regulation E. They also challenge the district court's separate holding that intrabank transfers preceding a fraudulent wire transfer are independently actionable as "unauthorized" electronic fund transfers, arguing that such transfers confer a net benefit on the consumer and produce no cognizable loss under the statute.

Divided Results from Other Courts

Since the lower court's ruling, several other courts have analyzed the issue and have reached divided results.

A federal court in South Carolina and one in Colorado have agreed with the court’s decision in the New York Case. In Walling v. Bank of America, 782 F. Supp. 3d 280 (D.S.C. 2025), the court adopted the reasoning of the New York Case and held that electronically initiated payment orders ancillary to wire transfers are covered by EFTA. Similarly, in Wingard v. TBK Bank, SSB, 768 F. Supp. 3d 1282 (D. Colo. 2025), the court relied on the New York Case to hold that intrabank transfers facilitating subsequent fraud could constitute unauthorized electronic fund transfers under EFTA.

A recent federal court in California, however, disagreed. In Jung v. Discover Bank, No. 25-cv-06383 (N.D. Cal. Mar. 9, 2026), the court expressly declined to follow the New York Case, reasoning that its "trifurcated transfer" analysis renders Section 7(B) superfluous because bank-to-bank transfers were already outside EFTA's coverage. The Jung court also noted that the 2010 Dodd-Frank extension of EFTA to remittance transfers would have been unnecessary under the NYAG's theory.

There are at least two other federal appellate court decisions that appear to directly disagree with the logic adopted by the New York Case. Both of these decisions preceded the New York Case but have held that wire transfers are exempt from EFTA. In Nazimuddin v. Wells Fargo Bank, the Fifth Circuit held that "EFTA regulations explicitly exclude wire transfers from the definition of an electronic fund transfer." Likewise, the Sixth Circuit in Wright v. Citizens Bank of East Tennessee, 640 F. App'x 401 (6th Cir. 2016), concluded that EFTA did not apply because "funds transfers … were made through Fedwire." The district court in the New York Case acknowledged these contrary authorities but distinguished them on the ground that none had considered the specific "trifurcated transfer" theory advanced by the attorney general in the New York Case.

The Second Circuit's decision will likely have substantial implications for the financial services industry. If the court affirms the lower court's ruling, banks may face liability under the EFTA and Regulation E, including strict reimbursement timelines, investigation requirements, and treble damages, for unauthorized consumer wire transfers long understood to be governed by Article 4A of the UCC. Such a result could require significant changes to bank operational procedures, loss-allocation frameworks, and consumer agreements. If the court reverses, it would preserve the longstanding regulatory framework under which Article 4A governs consumer wire transfers, providing banks with a commercially reasonable security procedure defense rather than the near-strict liability standard of the EFTA and Regulation E. Financial institutions and their counsel should monitor this case closely as the April 6, 2026, oral argument approaches.